Personal loans are commonly discussed in everyday conversations about money, yet many beginners are unsure what they really are or how they function. This article explains personal loans in a clear and simple way, without assumptions or technical language.

The goal is to help readers in the US and UK understand the concept, structure, and general mechanics of personal loans so they can recognize how they fit into the wider financial system.

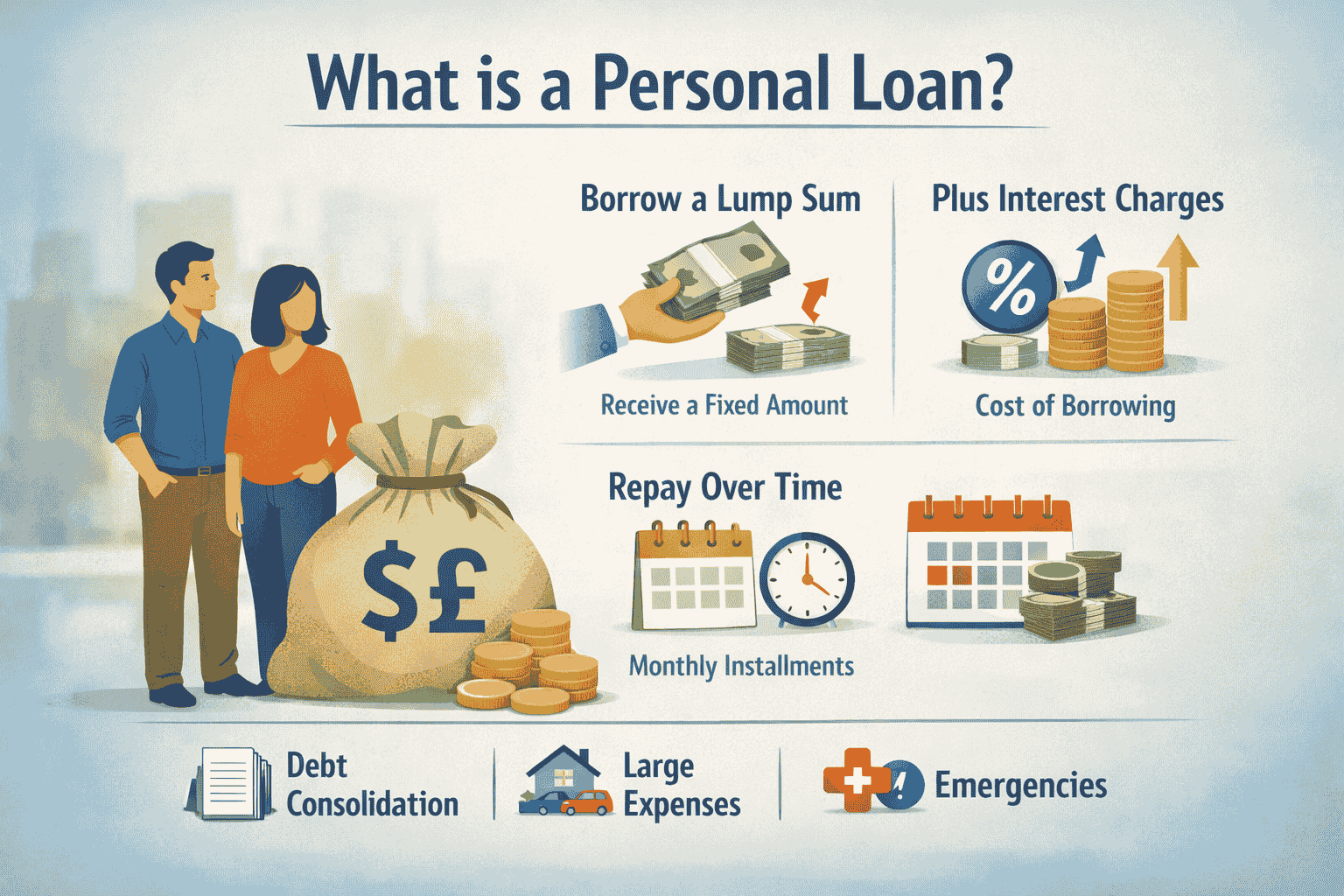

What Is a Personal Loan?

A personal loan is a type of borrowing where an individual receives a fixed amount of money and agrees to repay it over time. The repayment usually happens in regular installments, often monthly, over a set period.

Unlike some forms of borrowing that are restricted to a specific purpose, personal loans are generally flexible. This means the borrowed money can be used for many everyday needs, such as covering large expenses or managing temporary cash shortfalls.

Key Characteristics of a Personal Loan

A personal loan usually includes:

- A fixed loan amount

- A defined repayment period

- Regular repayment installments

- An interest charge added to the borrowed amount

These features make personal loans different from open-ended credit arrangements, where balances can go up and down frequently.

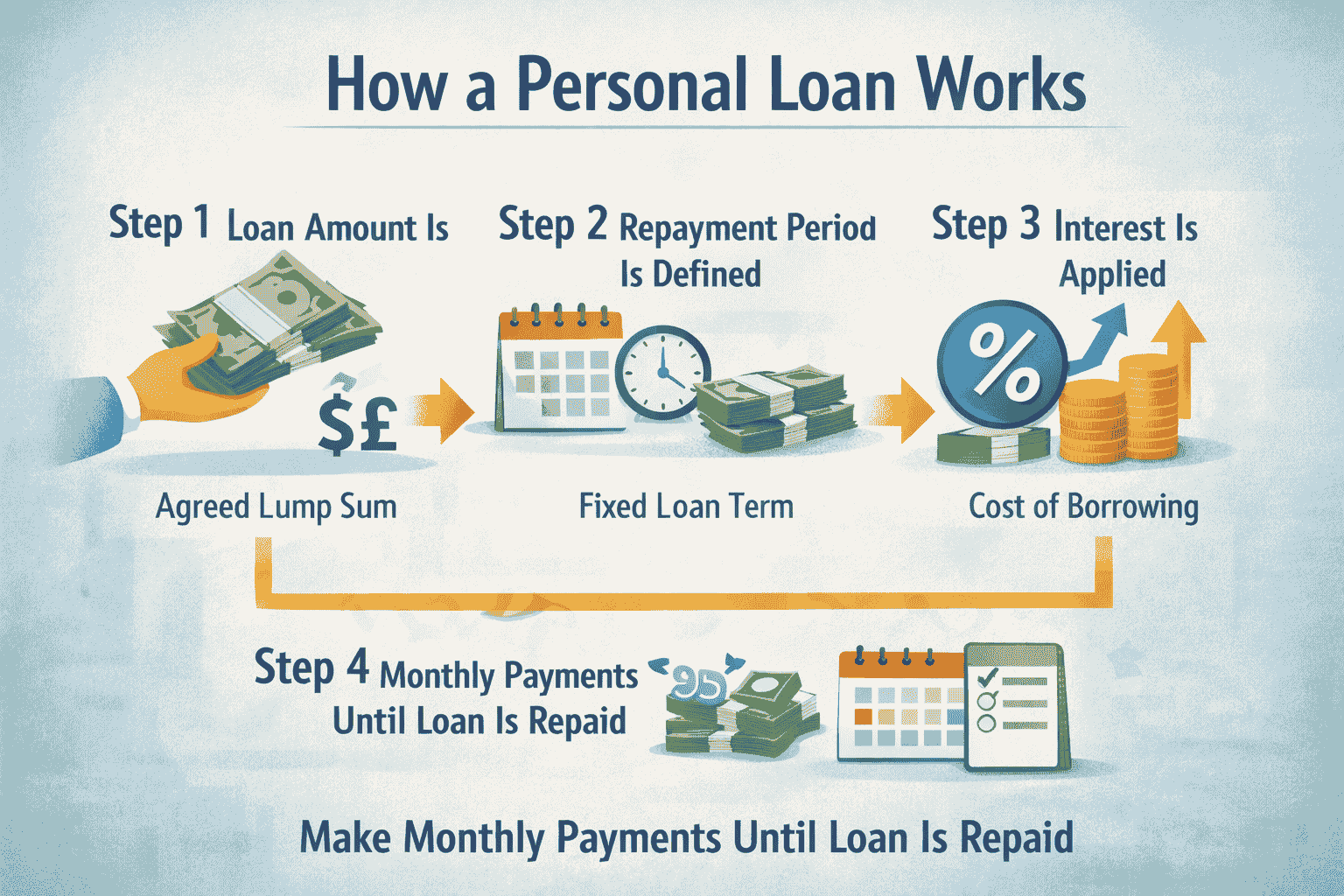

How a Personal Loan Works

At its core, a personal loan follows a simple process:

- A borrower receives a lump sum of money

- The borrower repays that amount gradually

- Interest is added as part of the total repayment

The structure is designed to be predictable, so borrowers know in advance how much they are expected to repay and for how long.

Step-by-Step Overview

Step 1: Loan Amount Is Set

The loan begins with a specific amount agreed in advance. This is the principal, or the original sum borrowed.

Step 2: Repayment Period Is Defined

The repayment period, sometimes called the loan term, is the length of time over which the loan will be repaid. This could range from a short period to several years.

Step 3: Interest Is Applied

Interest represents the cost of borrowing. It is calculated based on the loan amount and added to the total amount that must be repaid.

Step 4: Monthly Payments Begin

The borrower makes regular payments, usually monthly, until the loan is fully repaid.

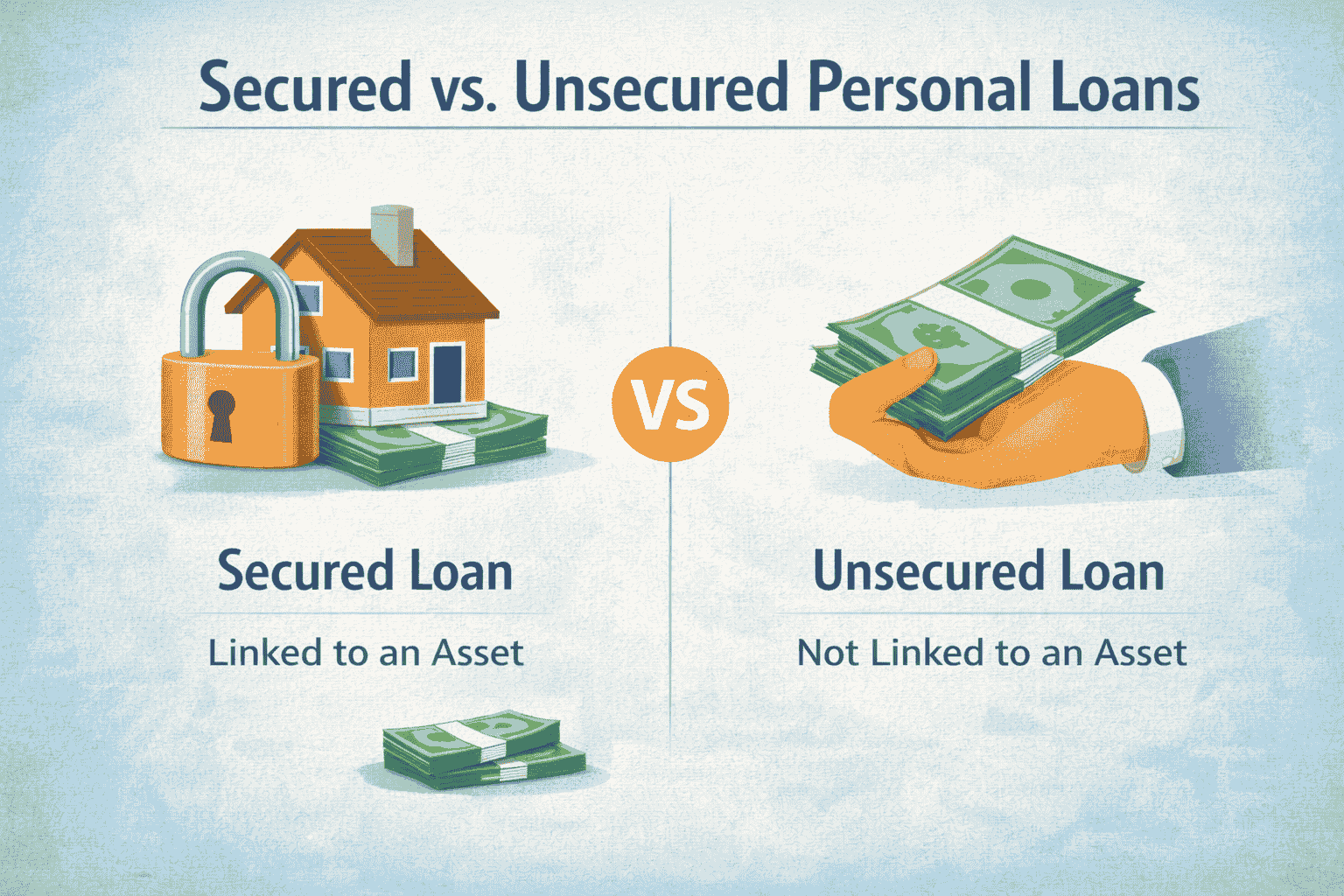

Secured vs. Unsecured Personal Loans

Personal loans generally fall into two broad categories based on whether something valuable is tied to the loan.

Unsecured Personal Loans

Unsecured personal loans do not require the borrower to provide an asset as security. Approval is typically based on factors such as income and credit history rather than physical property.

Because no collateral is involved, these loans rely heavily on the borrower’s ability and history of repayment.

Secured Personal Loans

Secured personal loans are linked to an asset, known as collateral. This could be something of value that supports the loan agreement.

The presence of collateral reduces risk for the lender, but it also means the asset is connected to the loan arrangement.

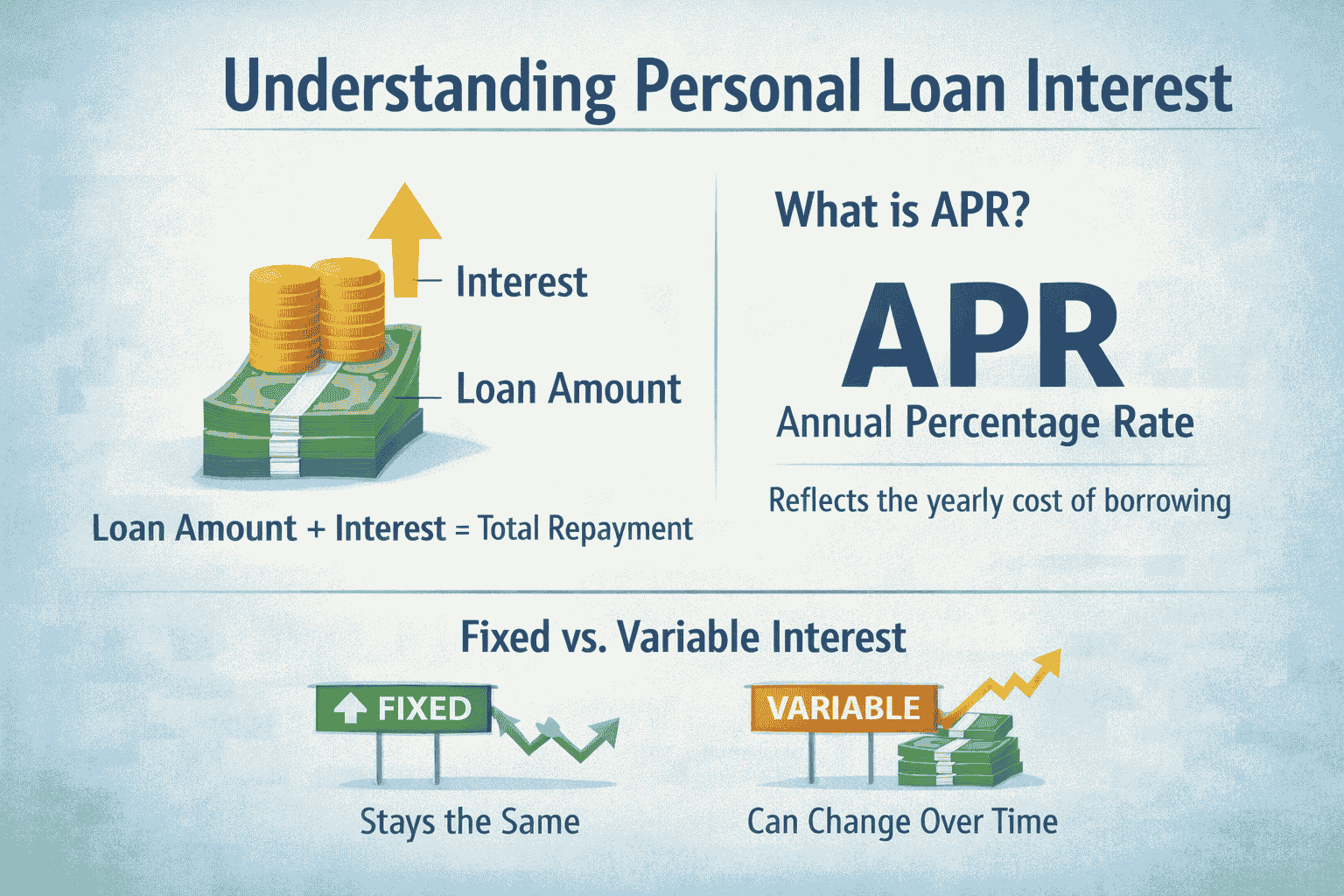

Interest Rates Explained in Simple Terms

Interest is the extra cost paid for borrowing money. It is often expressed as a percentage.

What Is APR?

APR stands for Annual Percentage Rate. It reflects the yearly cost of borrowing, including interest and certain fees. APR is commonly used to compare different borrowing options on a like-for-like basis.

Fixed vs. Variable Interest

- Fixed interest remains the same throughout the loan term

- Variable interest can change over time

Many personal loans use fixed interest, which helps keep repayments consistent.

Loan Repayments and Installments

Repayment is a central part of how personal loans work.

What Is a Monthly Installment?

A monthly installment is the regular amount paid toward the loan. It usually includes:

- Part of the original loan amount

- Part of the interest

Over time, the balance decreases until the loan is fully repaid.

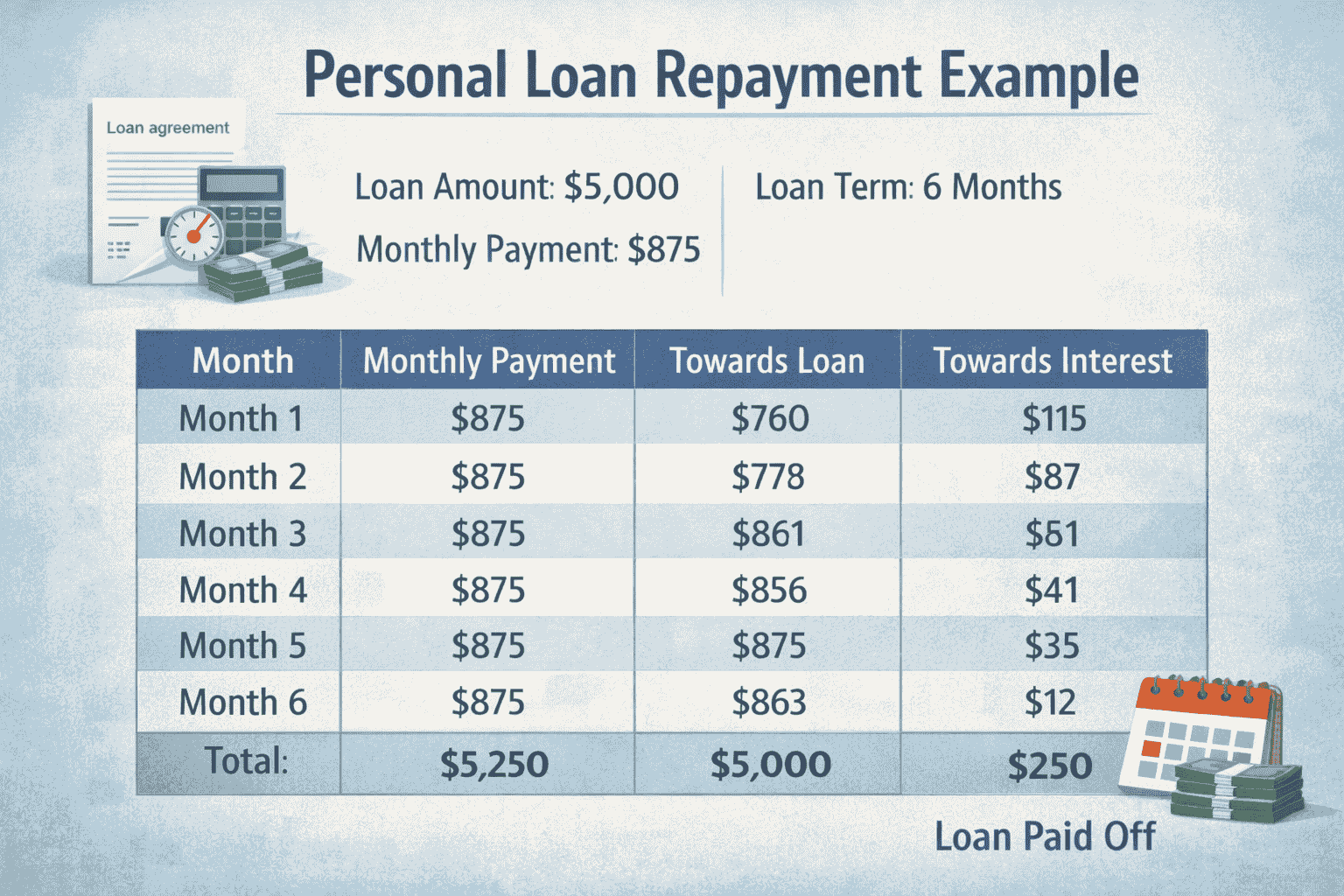

Example of Repayment Structure

Imagine borrowing a set amount to be repaid over several years. Each month, the same payment is made. Early payments may include more interest, while later payments focus more on reducing the remaining balance.

Common Uses of Personal Loans

Personal loans are often used for practical, everyday financial needs. Examples include:

- Covering large one-time expenses

- Consolidating multiple obligations into one payment

- Managing temporary financial gaps

The flexibility of personal loans is one reason they are widely discussed.

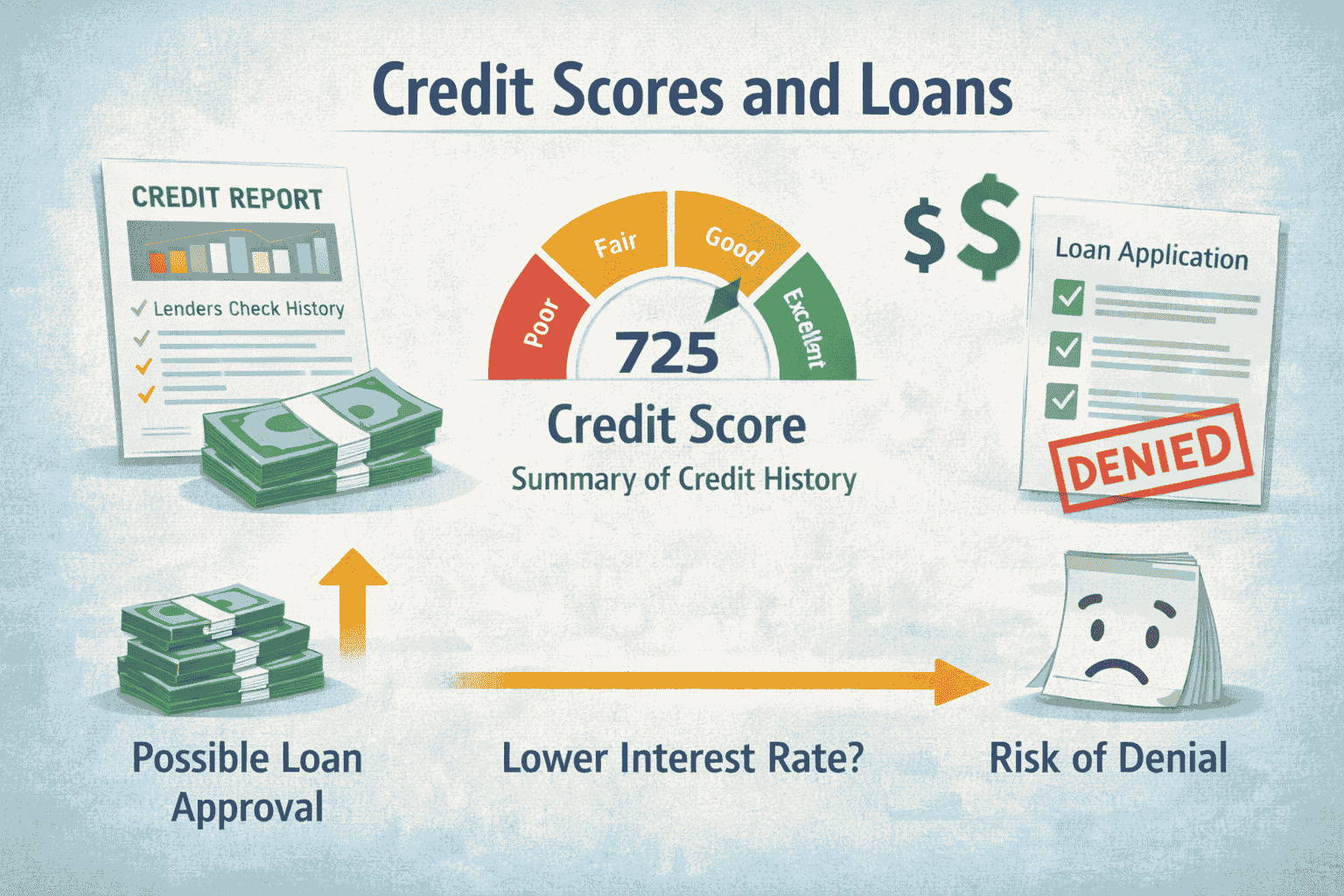

Credit Scores and Personal Loans

A credit score is a numerical summary of a person’s credit history. It reflects past borrowing behavior, such as repayment patterns and outstanding balances.

Why Credit Scores Matter

Credit scores help lenders assess how borrowing has been handled in the past. They can influence:

- Whether a loan is approved

- The interest rate applied

Credit scores do not tell the full financial story but are widely used as a reference point.

Fees and Additional Costs

Personal loans may include costs beyond interest. These can vary depending on the agreement.

Examples may include:

- Administrative fees

- Charges for missed payments

- Early repayment fees in some cases

Understanding these costs helps clarify the total repayment amount.

Differences Between Personal Loans and Other Borrowing Types

Personal Loans vs. Credit Cards

- Personal loans provide a lump sum upfront

- Credit cards allow ongoing borrowing up to a limit

Personal loans usually have fixed repayment schedules, while credit card balances can change month to month.

Personal Loans vs. Overdrafts

Overdrafts are linked to bank accounts and are typically used for short-term needs. Personal loans are structured for longer-term repayment.

Benefits of Personal Loans (Conceptual Overview)

From an educational perspective, personal loans are often described as:

- Structured and predictable

- Time-limited

- Easier to track due to fixed payments

These characteristics explain why they are commonly discussed in personal finance education.

Potential Limitations to Understand

It is also important to recognize limitations:

- Interest adds to the total cost

- Missed payments can have consequences

- Loans create ongoing obligations

- Understanding both sides helps build realistic financial awareness.

Frequently Asked Questions (FAQ)

What is a personal loan in simple terms?

A personal loan is borrowed money that is repaid in regular installments over a fixed period.

Do personal loans have to be used for one purpose?

Personal loans are generally flexible and not tied to a single specific use.

How long does a personal loan last?

The length depends on the agreed repayment period, which can vary widely.

Is interest always included in a personal loan?

Yes, interest is typically part of the total amount repaid.

Are personal loans the same in the US and UK?

The basic concept is similar, though terms and regulations may differ.

Educational Summary

A personal loan is a structured way to borrow a fixed amount of money and repay it over time with interest. It has clear terms, predictable payments, and a defined end date. Understanding how personal loans work helps beginners recognize how they fit into the broader financial system and how borrowing concepts are commonly explained.

This article is for educational purposes only.