Insurance is one of the most important financial tools people use to protect themselves from unexpected expenses. Whether it’s your home, car, health, income, or life, insurance provides a safety net when things go wrong. Yet many beginners feel confused by insurance terms, policy options, and coverage rules.

This guide explains insurance in clear, simple language. It covers how insurance works, why people use it, different types of insurance, common terms, myths, risks, and questions beginners often ask. By the end, you’ll understand the basics well enough to make informed decisions—without feeling overwhelmed.

What Is Insurance?

Insurance is a financial arrangement that protects you from large, unexpected expenses. In simple terms:

You pay a small amount (premium), and the insurance company agrees to help cover bigger costs if something goes wrong.

For example:

- You pay a monthly amount for auto insurance

- If your car is damaged in an accident, your insurance helps pay for repairs

Insurance does not prevent accidents or problems—but it reduces the financial impact.

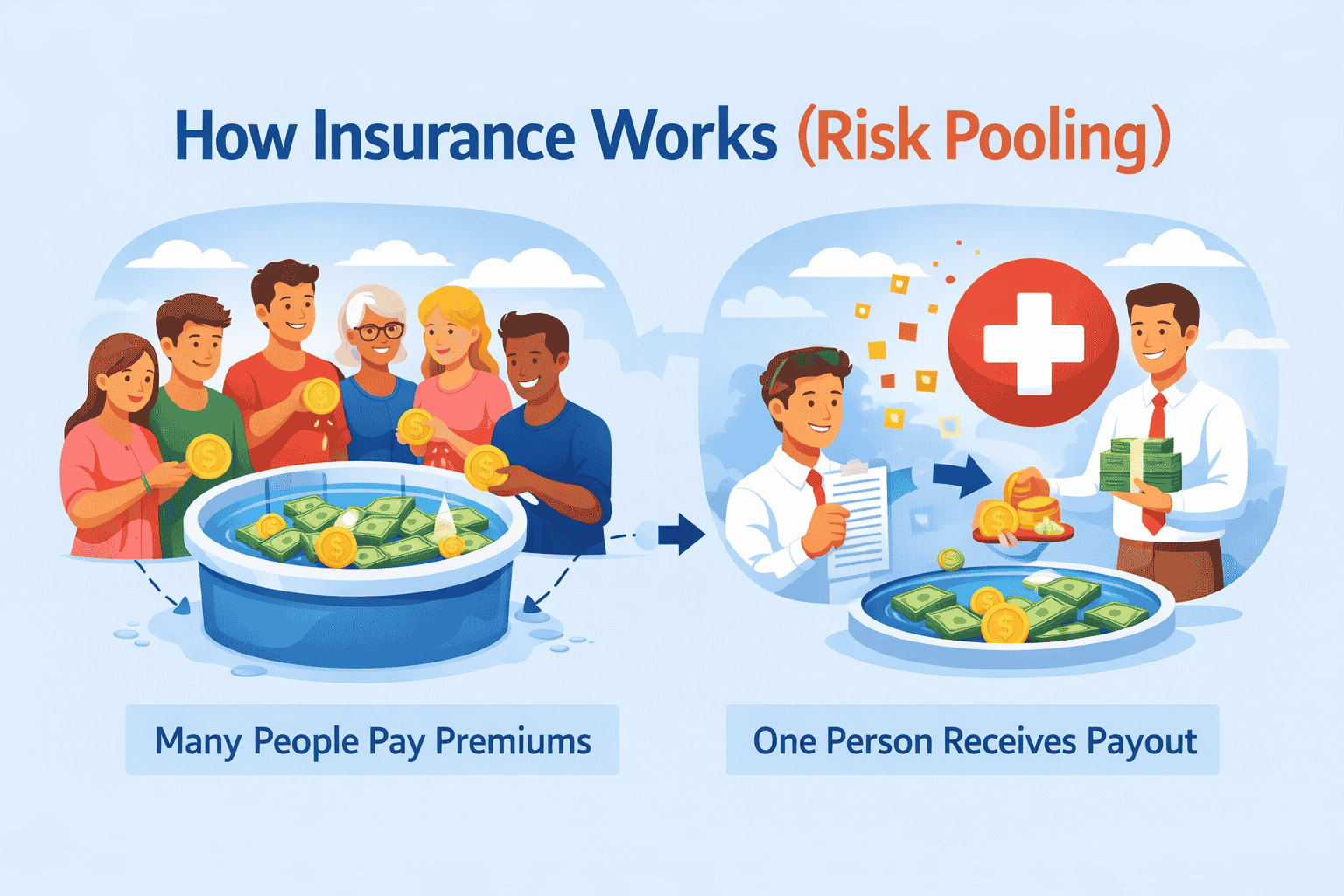

How Insurance Works

Insurance works through a concept called risk pooling.

The Basic Idea

Many people pay premiums into a shared pool. Only some of them will need help each year. The money in the pool is used to cover the losses of those who face unexpected events.

Key Steps in Insurance

1. You buy a policy

- You agree to the terms

- You pay premiums

2. You are covered for certain events

- Accidents

- Illness

- Property damage

- Loss of income

- Other risks depending on the policy

3. If something happens, you file a claim

- A claim is a formal request asking the insurer to pay for covered losses

4. The insurer reviews the claim

- They check if the event is covered

- They calculate how much to pay

5. The insurer pays the approved amount

Insurance does not cover everything. Every policy lists what is covered, what is not, and conditions required.

Why Insurance Matters

Insurance is important because it helps protect your finances from major losses.

Protection From Unexpected Costs

Without insurance, one accident, illness, or emergency could create thousands of dollars in expenses.

Peace of Mind

What Is Insurance? A Complete Beginner’s Guide to How Insurance Works

Knowing you are covered makes it easier to handle risks and uncertainties.

Helps You Manage Financial Planning

Insurance supports:

- Long-term stability

- Family protection

- Health planning

- Property protection

- Emergency management

Legal or Contract Requirements

Some insurance types are legally required in many places—for example, auto insurance in most US states.

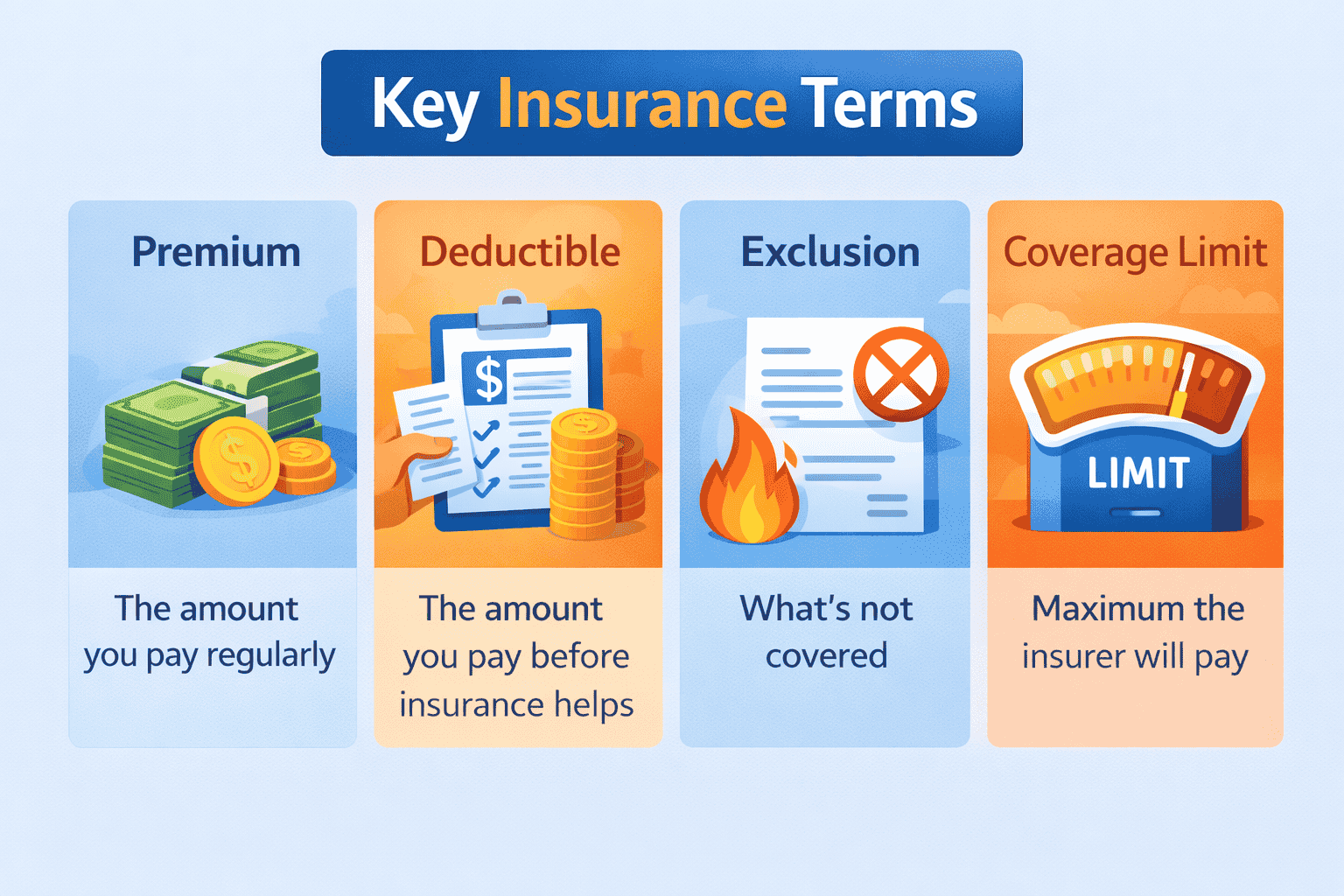

Key Insurance Terms Explained

Understanding insurance terminology helps you choose the right policy.

Premium

The amount you pay regularly (monthly or yearly) to keep the coverage active.

Deductible

The amount you pay out of pocket before insurance contributes.

Example:

If the deductible is $500 and a repair costs $2,000, you pay $500 and insurance pays the rest (depending on policy terms).

Copayment (Copay)

A fixed fee you pay for certain services (common in health insurance).

Coinsurance

A percentage of costs you share with your insurer after meeting the deductible.

Example:

You pay 20%, your insurer pays 80%.

Coverage Limit

The maximum amount the insurer will pay.

Exclusions

Events or situations not covered.

Policy

The contract explaining your coverage terms.

Claim

A request asking the insurer to pay for a covered loss.

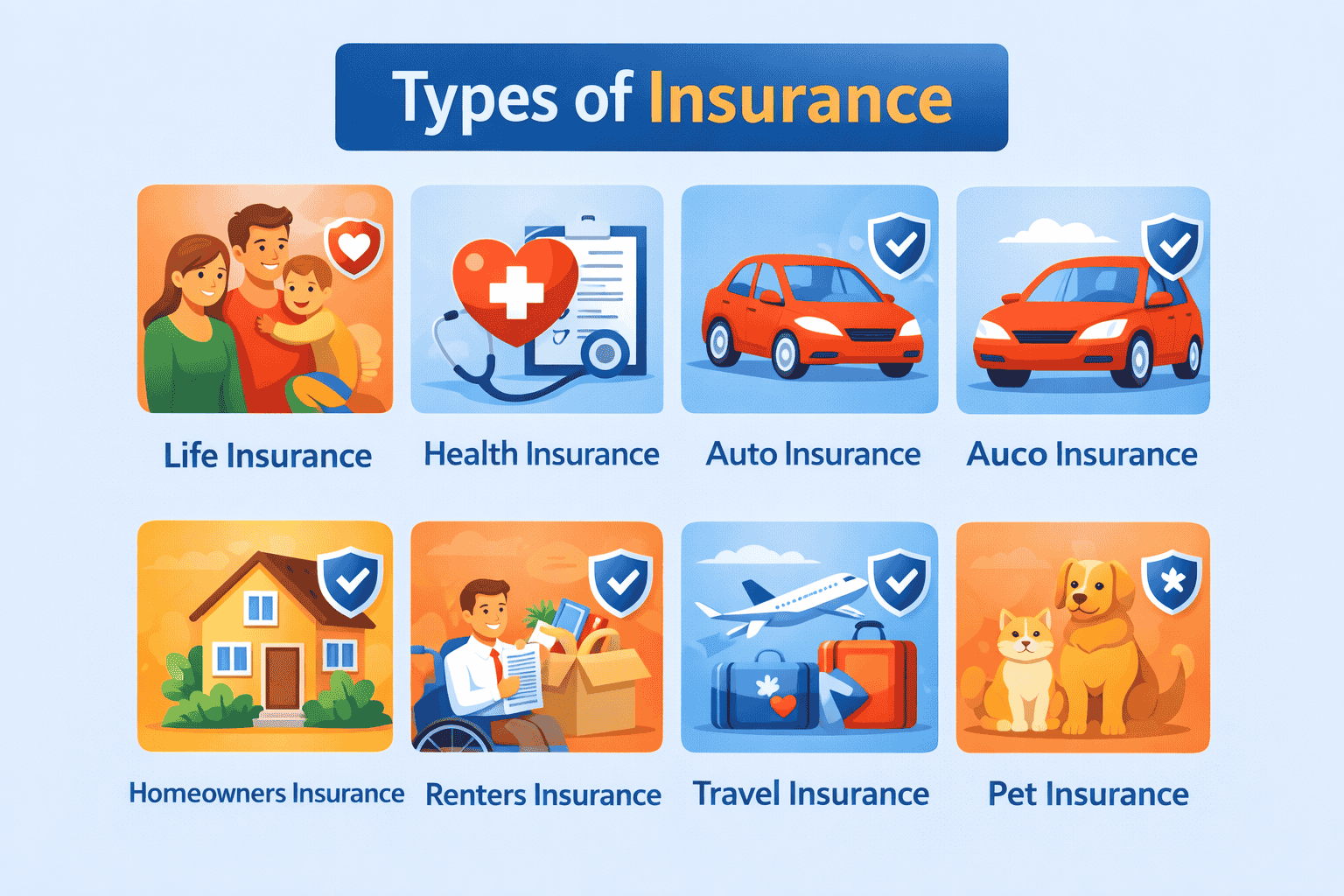

Types of Insurance

Below are the most common types of insurance individuals use.

A. Life Insurance

Life insurance provides financial protection for your loved ones if you pass away. It is often used to help cover:

- Household living expenses

- Funeral costs

- Children’s education

- Debt or mortgage payments

Types of Life Insurance

Term Life Insurance

- Covers a set number of years (10–30 years)

- Usually more affordable

- Pays out only if death occurs during the term

Whole Life Insurance

- Covers your entire lifetime

- Builds cash value over time

- Premiums are usually higher

Who May Consider It

- Parents

- Individuals with dependents

- People with financial responsibilities

B. Health Insurance

Health insurance helps cover medical expenses such as:

- Doctor visits

- Hospital stays

- Surgeries

- Prescriptions

Health care costs can be high, and insurance helps reduce the burden.

Common Features

- Deductibles

- Copayments

- Networks (specific doctors/hospitals covered)

Why It Matters

Even routine medical care can become expensive. Health insurance makes care more accessible.

C. Auto Insurance

Auto insurance protects you if you are involved in:

- A collision

- Vehicle damage

- Theft

- Injury-related costs

In many regions, drivers must have auto insurance to legally operate a vehicle.

Common Coverage Types

- Liability

- Collision

- Comprehensive

- Uninsured/Underinsured Motorist

D. Homeowners Insurance

Homeowners insurance protects your home and personal belongings.

Typically Covers

- Fire

- Theft

- Storm damage

- Personal liability

- Additional living expenses if your home becomes unlivable

Why It Matters

Homes are major financial investments. Insurance helps protect that investment.

E. Renters Insurance

Renters insurance covers your belongings if you rent a home or apartment.

Covers

- Theft

- Fire

- Some types of water damage

- Personal liability

Renters insurance is usually more affordable than homeowners insurance since it does not cover the building structure.

F. Disability Insurance

Disability insurance replaces part of your income if you cannot work due to illness or injury.

Two Types

Short-term disability (covers a shorter period)

Long-term disability (covers extended disability)

This type of insurance is often overlooked, but income protection can be essential for many individuals.

G. Travel Insurance

Travel insurance covers unexpected events during trips, such as:

- Trip cancellation

- Lost luggage

- Emergency medical costs

- Travel delays

It is especially useful for international travel.

H. Pet Insurance

Pet insurance helps cover veterinary bills for cats, dogs, and other pets. It often includes:

- Illnesses

- Accidents

- Surgeries

I. Business Insurance (Brief Overview)

Small businesses often use insurance to protect against:

- Property damage

- Liability claims

- Loss of income

- Employee-related risks

How Insurance Companies Evaluate Risk

Insurance companies use a process called underwriting to decide:

- Whether to offer coverage

- How much to charge

Factors Considered

- Age

- Health history

- Location

- Driving habits

- Dwelling characteristics

- Occupation

- Lifestyle choices

Insurance companies assess how likely an event is and price premiums accordingly.

What Affects Insurance Costs

Many factors influence the cost of insurance, including:

- Type of coverage

- Amount of coverage

- Deductible level

- Your risk profile

- Previous claims

- Location

- Policy features

Higher coverage generally means higher premiums. A higher deductible typically reduces premiums.

How to Compare Insurance Policies

When comparing policies:

1. Check coverage details

Understand exactly what is included and excluded.

2. Review deductibles

Higher deductibles reduce premiums but increase out-of-pocket costs.

3. Look at limits

Choose limits appropriate for your financial situation.

4. Understand the claims process

Look for clarity, simplicity, and reasonable timelines.

5. Compare premium costs

Price matters, but coverage quality matters more.

6. Evaluate customer service reputation

Service quality can make a big difference during a claim.

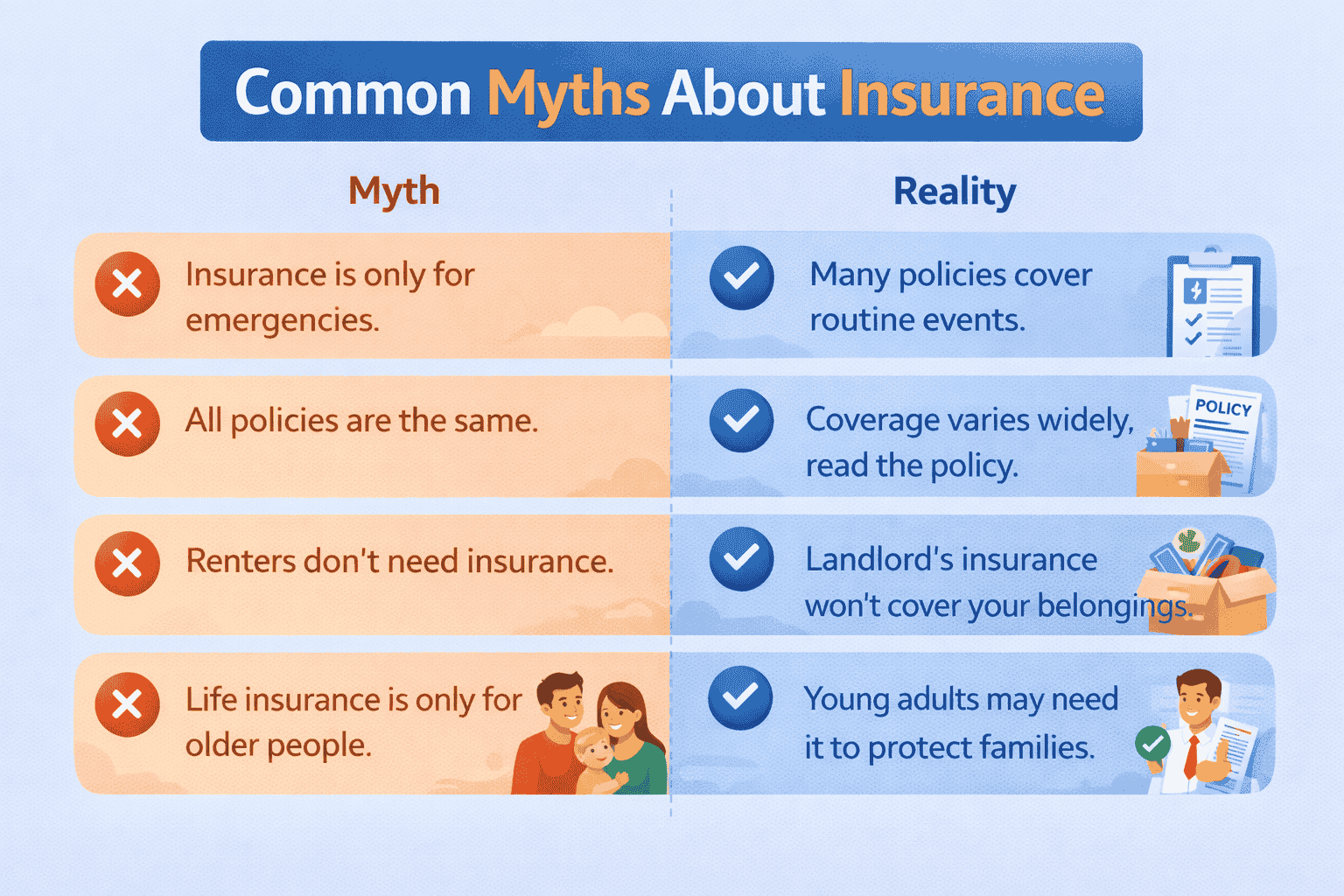

Common Myths About Insurance

Myth 1: “Insurance is only for emergencies.”

Many policies cover non-emergency events, such as checkups or minor repairs.

Myth 2: “All policies are the same.”

Coverage varies widely. Reading the policy is essential.

Myth 3: “Renters don’t need insurance.”

Your landlord’s insurance does not cover your belongings.

Myth 4: “Life insurance is only for older people.”

Many younger adults use it to protect family finances.

Myth 5: “Insurance companies always deny claims.”

Claims are denied only when the event is excluded or documentation is missing.

Mistakes to Avoid

- Not reading the full policy

- Choosing the cheapest plan without comparing coverage

- Ignoring exclusions

- Underinsuring property

- Not updating beneficiaries

- Forgetting to update coverage after major life changes

- Not keeping receipts or proof of ownership

When You Should Consider Buying Insurance

You may consider insurance when:

- You have dependents

- You own a home or car

- You have valuable belongings

- You want income protection

- You travel often

- You have pets

- You want protection from high medical costs

Insurance needs change over time, so regular review is helpful.

Frequently Asked Questions (FAQ)

1. Do I need insurance if I have savings?

Savings help, but unexpected events can be costly. Insurance adds another layer of financial protection.

2. Is insurance mandatory?

Some types—like auto liability coverage in many regions—may be required.

3. What happens if I miss a premium payment?

Coverage may lapse if payments stop. Policies typically explain grace periods.

4. Can I have multiple insurance policies?

Yes. Many people hold several types: auto, health, home, etc.

5. What is an insurance policy number?

A unique identifier used for claims and communication.

6. How long does a claim take?

It depends on the type of claim and required documents.

7. What is a beneficiary?

A person who receives the payout from life insurance.

8. Does insurance cover everything?

No. Policies always list exclusions.

Educational Summary

Insurance provides financial protection from unexpected events. By paying regular premiums, individuals reduce the financial impact of accidents, illnesses, property damage, and other risks. Different types of insurance serve different needs, and understanding terms like premiums, deductibles, limits, and exclusions helps beginners make informed choices. Always compare policies carefully and review your coverage regularly.

This article is for educational purposes only.