Credit cards are widely used financial tools in the US and UK. Many people use them for everyday spending, online purchases, travel bookings, and emergencies. However, for beginners, credit cards can feel confusing or even intimidating.

This guide explains what is a credit card , how it credit card works, and why people use it. The goal is to help you understand the concept clearly, without technical language or assumptions. No advice or recommendations are given—only education.

What Is a Credit Card?

A credit card is a payment tool that allows you to borrow money to make purchases. Instead of using your own money immediately, you use funds provided by the card issuer, which you repay later.

When you use a credit card:

- You are borrowing money

- You agree to repay what you borrow

- Repayment happens later, usually monthly

Think of a credit card as a short-term loan designed for everyday spending.

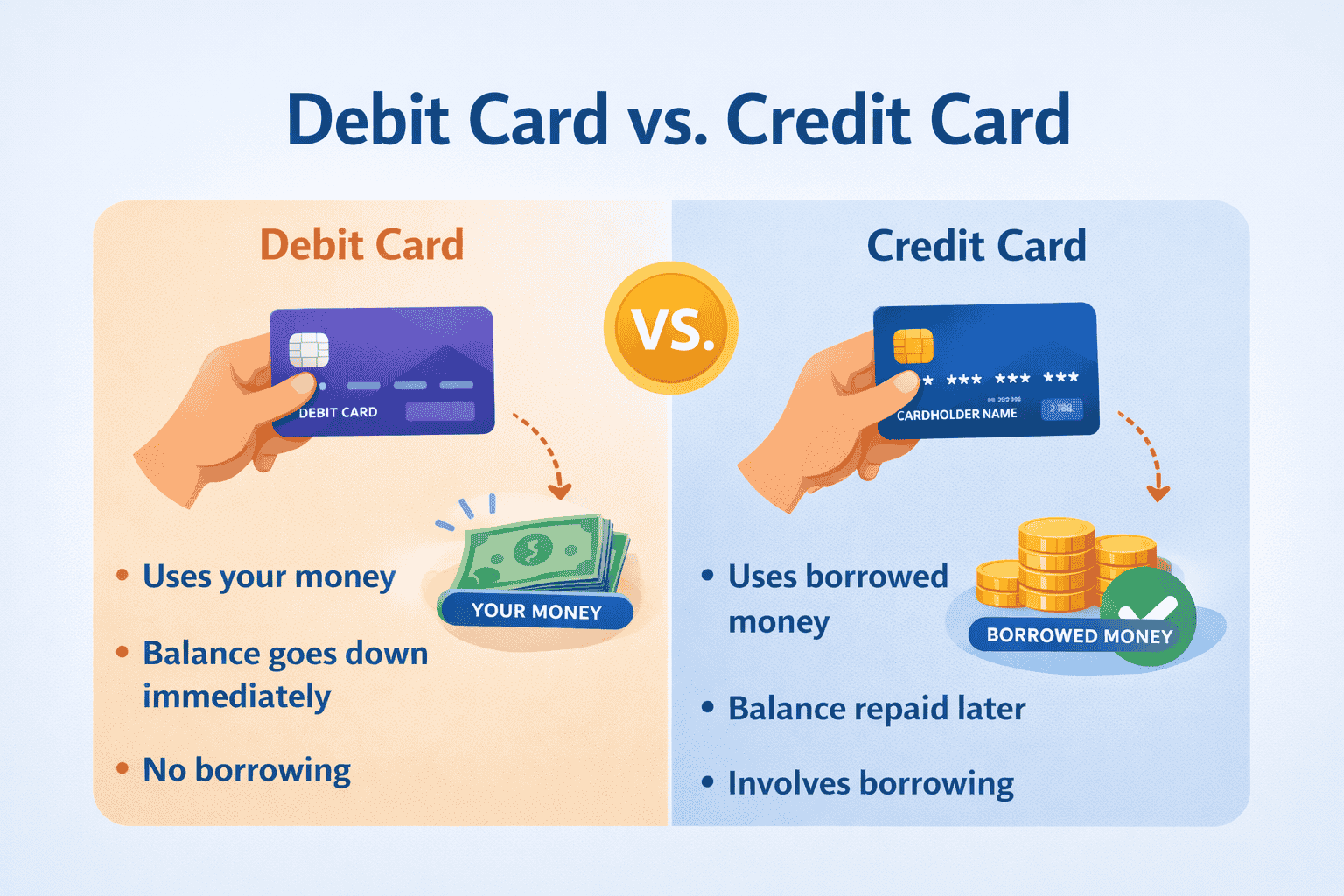

How Is a Credit Card Different From a Debit Card?

Understanding the difference between credit cards and debit cards is important.

Debit Card

- Uses money from your own bank account

- Balance goes down immediately after a purchase

- No borrowing involved

Credit Card

- Uses borrowed money

- Balance is repaid later

- Involves a credit limit and repayment rules

Example:

If you buy groceries for $50:

- With a debit card, $50 leaves your account right away

- With a credit card, you owe $50 and repay it later

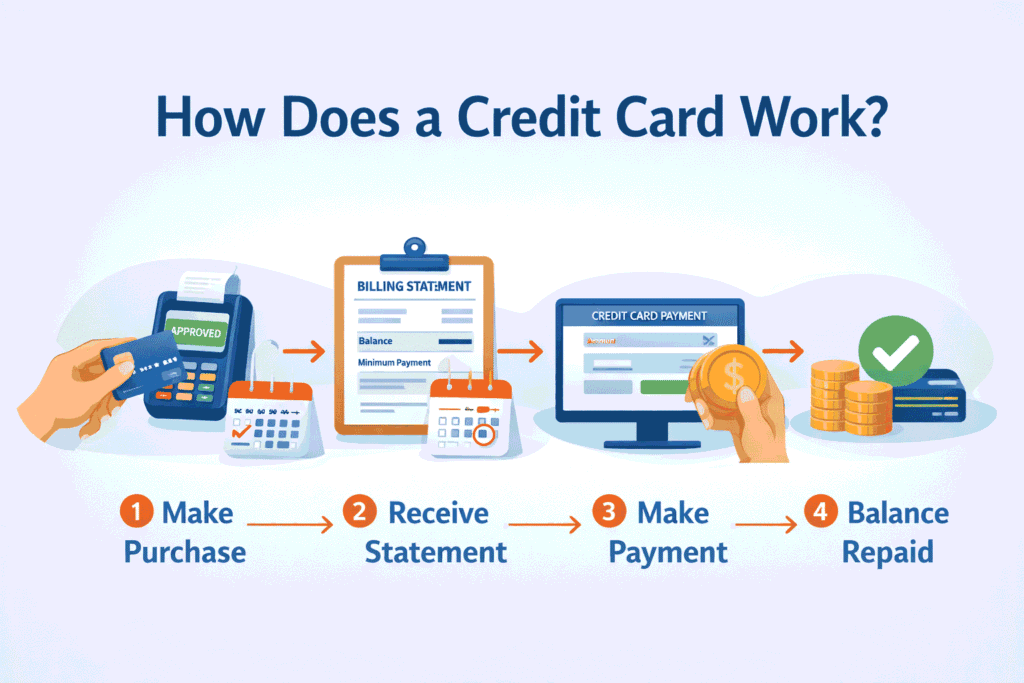

How Does a Credit Card Work?

Step-by-Step Example

- You make a purchase using your credit card

- The card issuer pays the merchant on your behalf

- The purchase amount is added to your credit card balance

- At the end of the billing period, you receive a statement

- You repay some or all of the balance by the due date

If the full balance is not paid, interest may apply.

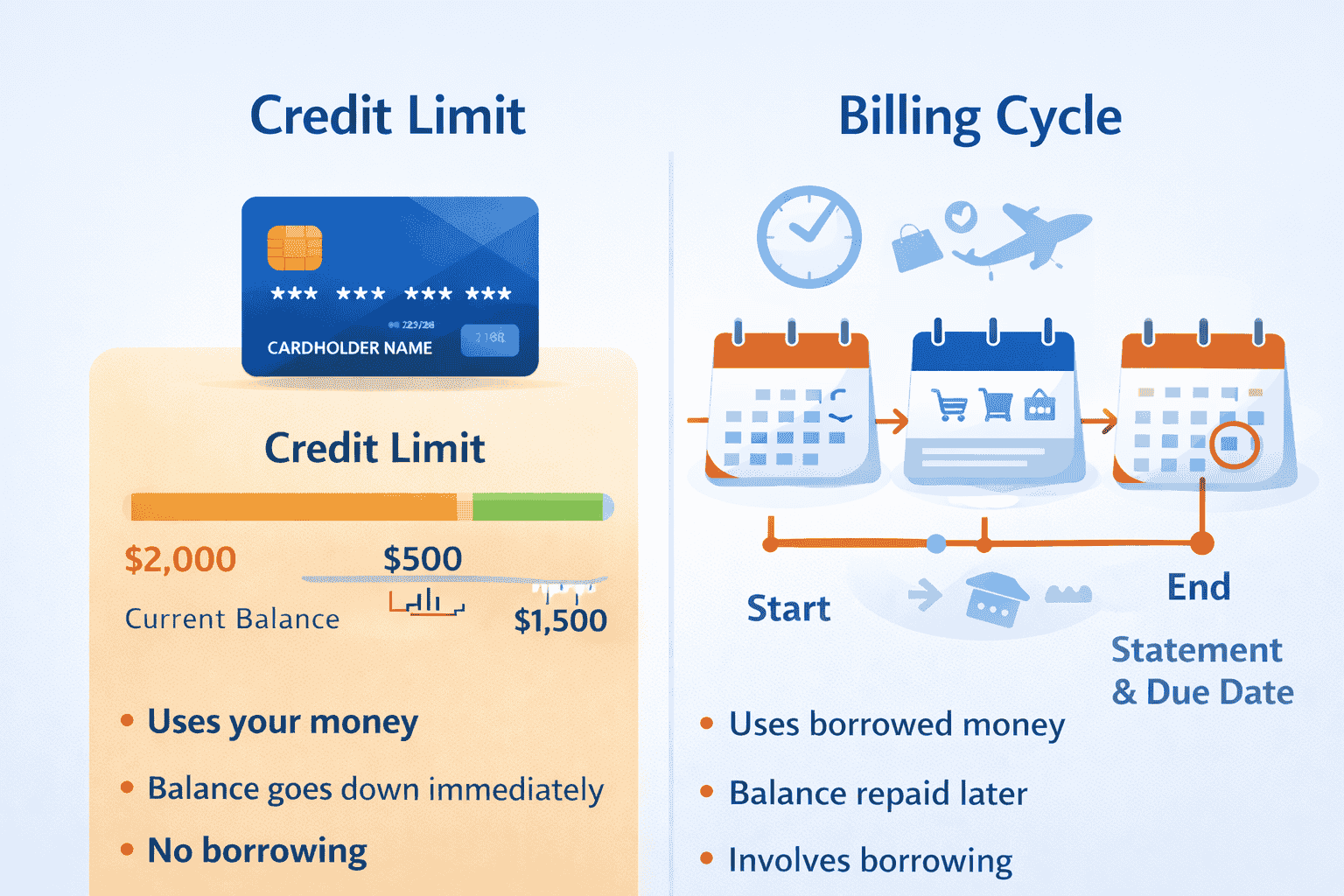

What Is a Credit Limit?

A credit limit is the maximum amount you are allowed to borrow on your card.

For example:

- Credit limit: $2,000

- Current balance: $500

- Available credit: $1,500

The limit is set by the card issuer based on factors such as income and credit history.

What Is a Billing Cycle?

A billing cycle is the period during which your purchases are recorded.

- Usually lasts about 28–31 days

- At the end of the cycle, a statement is generated

- The statement shows all transactions, balances, and due dates

Purchases made during one billing cycle appear on the next statement.

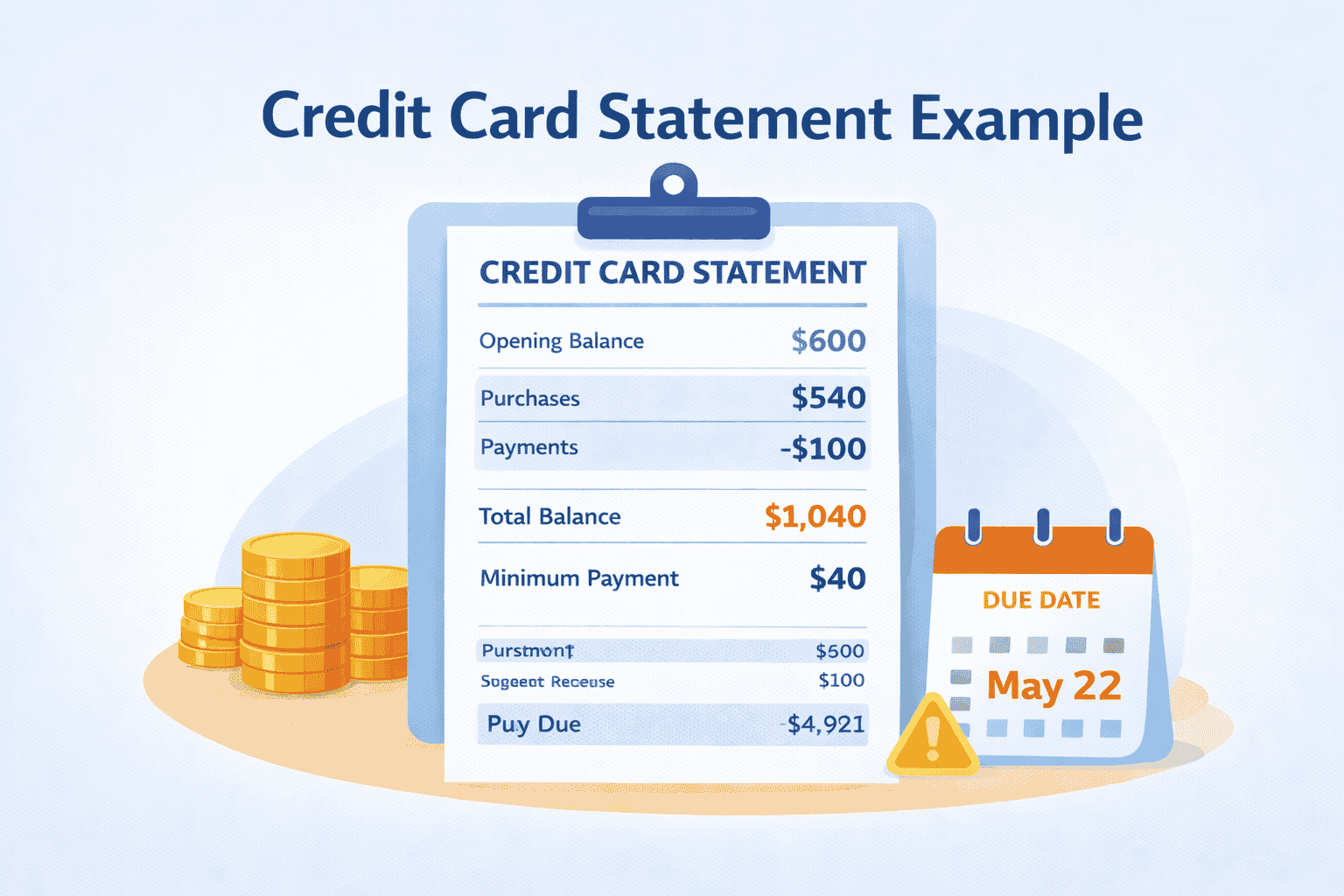

What Is a Credit Card Statement?

A credit card statement is a summary of your activity during the billing cycle. It includes:

- Opening balance

- List of purchases and payments

- Total balance owed

- Minimum payment amount

- Payment due date

Reviewing statements helps users understand spending and repayment.

What Is the Minimum Payment?

The minimum payment is the smallest amount you must pay by the due date to keep the account in good standing.

- Usually a small percentage of the balance

- Paying only the minimum means the remaining balance carries over

- Interest may apply to unpaid amounts

Paying more than the minimum reduces the balance faster.

What Is Interest on a Credit Card?

Interest is the cost of borrowing money.

If the full balance is not paid by the due date:

- Interest may be added to the remaining amount

- Interest is calculated as a percentage

This is why understanding repayment terms is important for credit card users.

What Is an Annual Percentage Rate (APR)?

APR stands for Annual Percentage Rate. It represents the yearly cost of borrowing money on a credit card.

- Expressed as a percentage

- Applied to unpaid balances

- Can vary depending on card terms

APR helps explain how interest builds over time.

Why Do People Use Credit Cards?

People use credit cards for many practical reasons.

Convenience

Credit cards are widely accepted and easy to use for both in-store and online purchases.

Cash Flow Management

They allow purchases even when immediate cash is not available, with repayment later.

Record Keeping

Statements provide detailed records of spending.

Online and Travel Use

Credit cards are often required for online services, reservations, and bookings.

What Is Credit Utilization?

Credit utilization refers to how much of your available credit you are using.

Example:

- Credit limit: $1,000

- Balance: $300

- Utilization: 30%

Lower utilization generally shows controlled borrowing behavior.

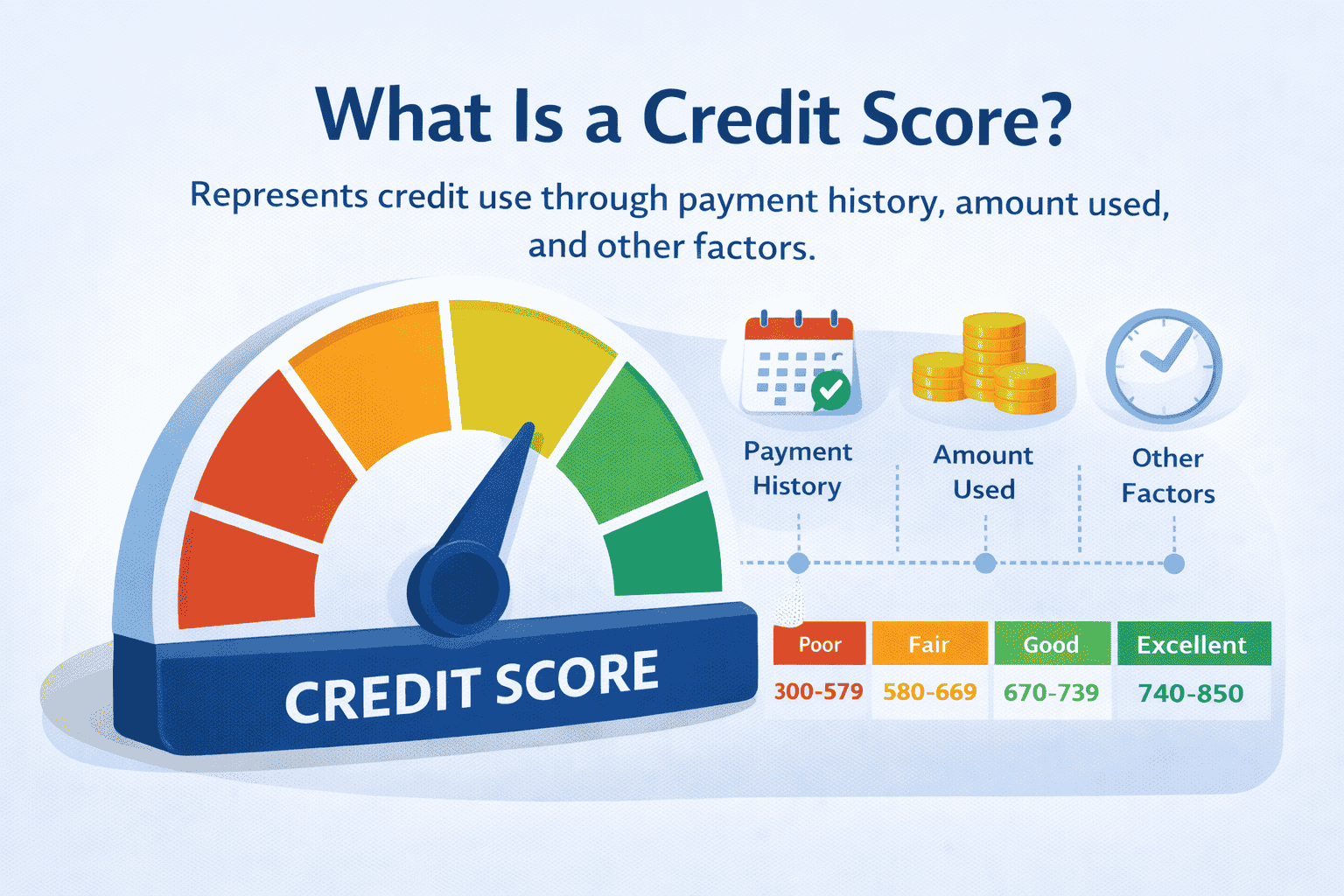

What Is a Credit Score?

A credit score is a number that represents how a person has used credit in the past.

Credit card activity can influence this score through:

- Payment history

- Amount of credit used

- Length of credit history

Credit scores are commonly used in the US and UK to assess credit behavior.

How Do Payments Affect Credit History?

Payments are recorded over time and form part of a credit history.

- Paying on time shows reliability

- Missing payments may be recorded negatively

- Long-term patterns matter more than single events

Understanding this helps explain why repayment habits are important.

What Are Fees Associated With Credit Cards?

Credit cards may include different types of fees, depending on terms.

Common Fee Types

- Annual fees

- Late payment fees

- Foreign transaction fees

Not all cards have all fees. Terms are outlined in card agreements.

What Happens If a Payment Is Late?

Late payments can lead to:

- Late fees

- Added interest

- Negative impact on credit history

Due dates are clearly stated on statements to help avoid this.

What Is a Cash Advance?

A cash advance allows users to withdraw cash using a credit card.

Key points:

- Treated differently from purchases

- Often has higher interest

- Interest may start immediately

Cash advances are generally used differently than regular spending.

Are Credit Cards the Same in the US and UK?

The basic concept is the same in both regions:

- Borrowing money

- Repayment later

- Interest on unpaid balances

However, details such as regulations, fees, and reporting systems can differ slightly.

What Is Responsible Credit Card Use?

Responsible use means understanding how the card works and managing it carefully.

Key ideas include:

- Tracking spending

- Paying attention to statements

- Knowing due dates

These habits help users stay informed about their finances.

Common Credit Card Myths

Myth 1: Credit cards are free money

Reality: They involve borrowing and repayment.

Myth 2: You must carry a balance

Reality: Paying in full avoids interest.

Myth 3: Credit cards are only for emergencies

Reality: They are used for many everyday purposes.

How Can Beginners Learn to Manage Credit Cards?

Beginners can focus on:

- Reading statements carefully

- Understanding terms and fees

- Starting with small purchases

- Monitoring balances regularly

Learning happens over time with experience.

Frequently Asked Questions (FAQ)

What happens if I never use my credit card?

The account remains open, but inactivity rules vary. Some issuers may close inactive accounts.

Is a credit card the same as a loan?

A credit card is a type of revolving credit, which differs from fixed loans with set repayment schedules.

Can I use a credit card internationally?

Many cards can be used abroad, though currency conversion rules and fees may apply.

Do credit cards expire?

Yes, cards have expiration dates printed on them. Replacement cards are usually issued before expiration.

Can I have more than one credit card?

Some people have multiple cards, each with its own limit and terms.

Key Terms to Remember

- Credit limit – Maximum amount you can borrow

- Billing cycle – Period when transactions are recorded

- Statement – Summary of account activity

- Minimum payment – Smallest required payment

- Interest – Cost of borrowing money

Understanding these terms makes credit cards easier to manage.

Educational Summary

A credit card is a tool that allows people to borrow money for purchases and repay it later. It works through billing cycles, statements, and repayment rules. While credit cards offer convenience and flexibility, they also require understanding how borrowing, interest, and payments work. For beginners, learning the basics helps build confidence and financial awareness over time.

This article is for educational purposes only.